Reports and articles

From rapid growth to slowdown: how structural change reshaped China’s economy

Published on March 17th 2026

By Zongshuai Fan, Cambridge Industrial Innovation Policy

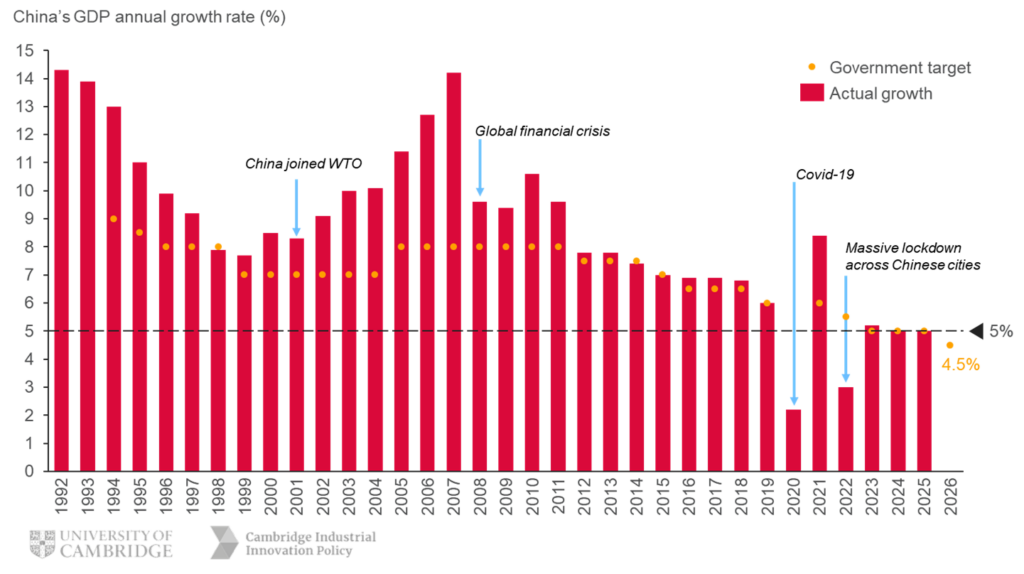

China is now the world’s second-largest economy. In 2024, its GDP reached 134.9 trillion yuan (about US$18.8 trillion), roughly two-thirds the size of the US economy. Yet since the early 2010s, growth has clearly slowed, with annual expansion settling into a lower range in recent years.

As China’s 2026 Government Work Report was released in early March, it confirmed that the economy grew by 5 per cent in 2025, right meeting the target set a year earlier. The report also set a 4.5 to 5 per cent growth target for 2026. It is the lowest GDP annual growth goal Beijing has set in decades.

Figure 1: China’s GDP actual growth and government target, 1992–2026

Source: International Monetary Fund, IMF (2025). People’s Republic of China (accessed 11 July 2025); State Council of the People’s Republic of China (1994-2026). Report on the Work of the Government

How should we understand the forces behind China’s rise, the loss of momentum, and the country’s future trajectory? Our new policy paper addresses these questions through the lens of structural change. It examines how the role of different sectors in the Chinese economy has evolved over the past three decades, and how this transformation has shaped both rapid growth and the subsequent slowdown.

The policy paper is part of a broader series on how sectoral change influences national economic performance across different contexts. Focusing on China, it traces the country’s structural evolution and explores the reforms and industrial policies that have helped shape its economic trajectory.

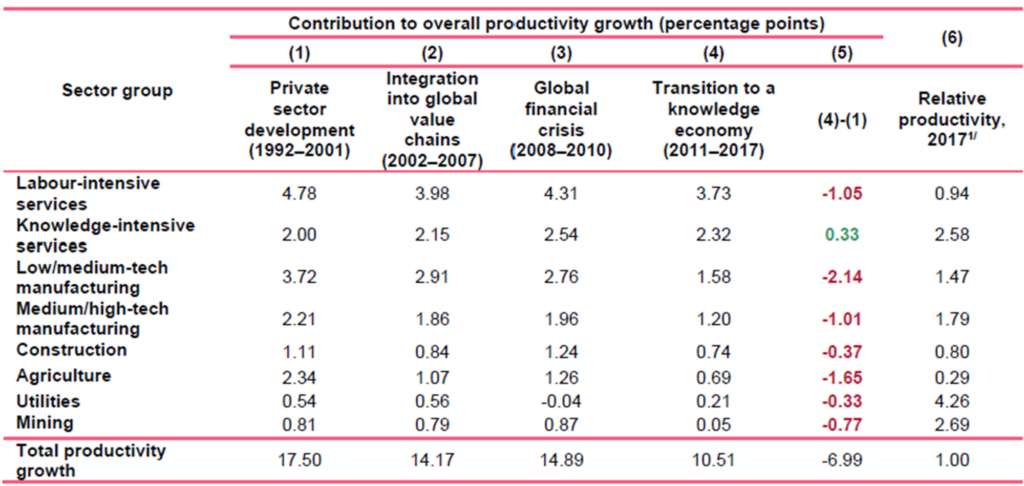

From 1992 to 2007, China’s economic growth was driven by productivity gains across all sectors and the shift of workers to higher-productivity sectors

Between 1992 and 2007, China experienced some of its fastest growth, largely driven by productivity improvements across all sectors and the expansion of low/medium-tech and medium/high-tech manufacturing, alongside labour-intensive services.

The most significant productivity gains from the reallocation of workers from low- to high-productivity sectors occurred between 2002 and 2007. During this period, over 52 million agricultural workers shifted primarily into labour-intensive services and manufacturing industries.

This sectoral shift contributed 2.4 percentage points to the overall productivity growth. More than half of these gains were derived from the manufacturing sector. Between 2002 and 2007, employment in low/medium-tech manufacturing increased by 19.9 million workers, while medium/high-tech manufacturing saw a rise of 12.8 million workers. Key manufacturing industries that increased their employment include: apparel and textiles, electronic and telecommunication equipment, food products, electric equipment and machinery and equipment.

The contraction and slowdown of low/medium-tech manufacturing accounts for nearly a third of China’s economy slowdown since the 2010s

As international trade slowed down after the global financial crisis of 2008/09, and China prioritised the development of its medium/high-tech manufacturing and knowledge intensive services, the role of low/medium-tech manufacturing in the Chinese economy has diminished.

Although sectors such as construction and mining faced more pronounced slowdowns, the relatively larger size of low/medium-tech manufacturing both in terms of employment and value added (11.2% and 17.2% in 2017), meant that its contraction and deceleration had a more significant impact on the overall economy. This sector group experienced the largest decline in its contribution to productivity growth during the 2011 ̶ 2017 period, compared to the 1992 ̶ 2001 period. This decline accounted for nearly a third of the overall slowdown of the Chinese economy (Table 1).

The textiles and apparel industries were key contributors to this deceleration, accounting for 28% of the reduction in the contribution of low/medium-tech manufacturing to overall productivity growth during the 2011 ̶ 17 period, compared to the 1992 ̶ 2001 period.

The expansion of labour- and knowledge-intensive services has not been able to offset the decline of low/medium-tech manufacturing

After 2010, knowledge- and labour-intensive services became the primary sectors attracting workers from other industries. As employment shares in mining, low/medium-tech manufacturing and agriculture declined, labour-intensive services expanded more rapidly than in previous periods, increasing their employment shares by 5.8 percentage points from 2011 to 2017.

During this period, the employment share of knowledge-intensive services also saw a substantial increase, rising from 5.1% in 2011 to 8.3% in 2017. This growth, combined with productivity levels above the national average, led to knowledge-intensive services surpassing low/medium-tech manufacturing in their contribution to GDP growth for the first time, with contributions of 21.9% and 15.1%, respectively. Key contributors to this growth within knowledge-intensive services include: financial intermediation (7.2%), leasing, technical, science, and business services (7%), and postal and telecommunications services (3.9%).

This shift has important implications for the future growth of China’s economy. Although knowledge-intensive services have productivity levels more than twice the national average, their relatively small size has limited their ability to offset the slowdown in other sectors. Meanwhile, labour-intensive services, which employ more than a third of the workforce, have productivity levels below the national average (relative productivity lower than “1”) and lower than those of manufacturing industries (Table 1).

Table 1: Contribution to productivity growth by sector group, 1992-2017

Source: RIETI (2023). China Industrial Productivity Database 4.0. (accessed 11 June 2024)

In the years following 2017, China’s economic growth decelerated further, averaging 5.3% annually between 2018 and 2022. Despite this slowdown, China’s growth rate remained significantly higher than that of advanced economies, which averaged 1.7%, and emerging and developing economies, which averaged 3.5% during the same period.

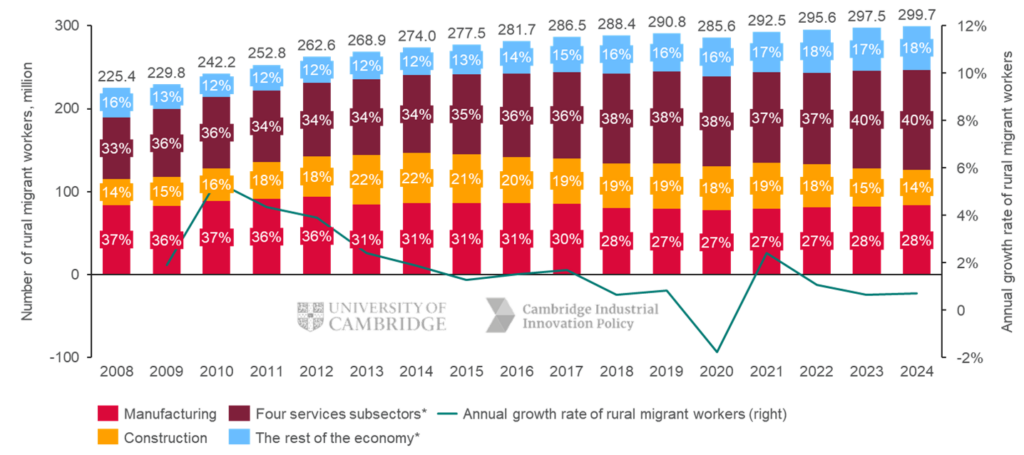

Our analysis provides evidence of a declining structural bonus (productivity gains from workers moving from lower- to higher-productivity sectors) as a key factor in China’s economic slowdown since 2011. As more sophisticated industries expand their participation in the economy, rural migrant workers are increasingly moving to lower-productivity service sectors rather than low/medium-tech manufacturing roles, which have higher productivity levels. This is particularly relevant because agriculture workers still accounted for 22% of the total workforce in 2021, representing approximately 165 million people.

Figure 2: Number of rural migrant workers by sector and annual growth rate, 2008–2024

Note: Four services subsectors include 1) wholesale and retail trades, 2) transport, storage and post, 3) accommodation and catering services and 4) service to households and repair. The rest of the economy includes mining, public utilities and the rest of services sectors (i.e. finance, education, administrative services, and health).

Source: China’s National Bureau of Statistics. National Survey Report on Rural Migrant Workers (Year 2012-2024)

Looking ahead: perspectives for future growth

Our study underscores the ongoing influence of industrial policy in shaping China’s economic performance. Developing productive forces and engaging in global trade and investment remain widely emphasised across China’s policies. In September 2023 Xi Jinping proposed the concept of “New Quality Productive Forces”, highlighting the importance of innovation, technology and the manufacturing sector in China’s future economic development.

What can be expected for China’s future economic performance? Our sectoral analysis indicates that, as the manufacturing sector slows its expansion and rural migrant workers increasingly move into labour-intensive services, it is unlikely that ongoing structural change will sustain double-digit growth rates in the future. However, recent economic performance and policy developments also suggest that China’s growing leadership in innovation and technology may enable the country to maintain growth rates above those of most emerging and advanced economies.

Get in touch to find out more about working with us